Quater Report of 2010

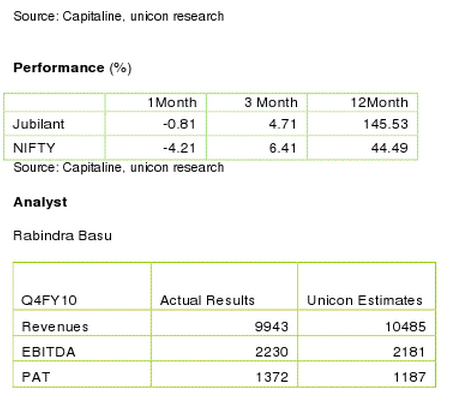

Net sales in Q4FY10 stood at INR 9943 mn vs INR 8437 mn,

in increase by 18% in-line with Unicon’s estimate of INR

10485 mn

Pharmaceuticals & Life sciences Products & Services

(PLSPS) business has grown by 20.5% driven by CRAMS

grew by 16.8% on back of strong volumes based on

delivery from new contracts

Revenues from the Agri & Performance Polymers (APP)

business were tepid on back of decline in revenues of its

Polymers & Fertilizer business

EBIDTA stood at INR 2230 mn vs INR 954 mn in-line with

Unicon’s estimate of INR 2181 mn

Margins at 22.4%, an increase by 1110 bps Y-o-Y on

account of margin improvement in Proprietary products, API,

generics, Life Science Chemicals, DDDS business and

normalcy in APP margins

PAT at INR 1372 mn against INR 124 mn in Q4FY09 and

margins at 10.3% above Unicon’s estimate of INR 1187 mn

Jubilant raised INR 3870 mn through QIP which has led to

in debt/equity ratio to 1:1

By Q3FY11 the company expects to complete demerger of

Agri and Performance Polymer business

Valuation and outlook

At CMP of INR345 the stock is trading at a PER of 10.4x FY11E

EPS of INR 33. Considering an earnings CAGR of 15% over

FY08-11E we do not expect a PE contraction from the current

level. In fact improving return ratios backed by a strong earnings

growth for the next two years would support PE expansion.

PLSPS business seems to be gaining traction with increased

revenue visibility of CMO sterile and DDDS. Going forward the

company would complete the demerger of its APP and high

margin PLSPS business which would lead to value unlocking.

3 comments:

Excellent report

curry shoes

golden goose outlet

hermes outlet

curry 9

off white

gy648ghhc

golden goose outlet

golden goose outlet

golden goose outlet

golden goose outlet

golden goose outlet

golden goose outlet

golden goose outlet

golden goose outlet

golden goose outlet

supreme outlet

Post a Comment